RegZ - LE

Working with 2015 RESPA-TILA Regulations

The RegZ-LE provides an overall view of the terms of the loan and its costs over time. Changes to fields on the RegZ-LE are reflected on the 1003 and Loan Estimate input forms as appropriate. If you have completed the 1003 application for the borrower or copied values from a Loan Program template, many of these fields are already filled. The RegZ-LE has no corresponding output form and is used primarily to review loan information and to enter or edit information about specific types of loans (for example, ARM mortgages).

This help topic describes the 2015 Loan Estimate form required by RESPA regulations for loans originated on or after October 3, 2015. Your Encompass administrator configures when your company switches by default from the 2010 to the 2015 forms. However, if you have not yet sent your initial disclosure to the borrower, you can switch between the 2010 and 2015 versions of the forms by clicking Forms on the Encompass menu bar, pointing to RESPA-TILA Form Version, and then clicking the 2010 or 2015 option. To view the help topic for the 2010 REGZ-TIL disclosure form, refer to the RegZ Truth-in-Lending Disclosure help topic.

Section Information

-

Most of the fields in the top section are populated automatically based on information entered in the Disclosure Tracking tool when disclosures are made to the borrower.

-

For the Loan Program, click the Find icon to select a template of predefined loan terms and values.

-

For the Closing Cost Program, click the Find icon to select a template that calculates the closing costs using predefined rates and values.

-

If the information is not already populated, type the 1st Payment Date used to calculate the payment and aggregate escrow account schedules, or click the Calendar icon to select a date.

The basic loan amount and terms should be populated from the Borrower Summary form. If not, enter that information plus any additional terms required for the type of loan being created. For example, rates for Buydown and ARM mortgages, biweekly payments, potential negative amortization, and construction mortgage details.

Enter the loan amount, followed by the additional terms required for the loan.

Enter the number of months that payments will be applied to the interest rate only. Select the Qualify using P&I checkbox to qualify the loan using an estimated payment that includes both principal and interest.

Select a method of calculation for the repayment schedule. For each option, the value represents the number of days per year used to calculate the loan's daily interest.

Select the checkbox to require mortgage payments every two weeks, rather than every month. For more information about biweekly loans, refer to the Process a Biweekly Loan topic.

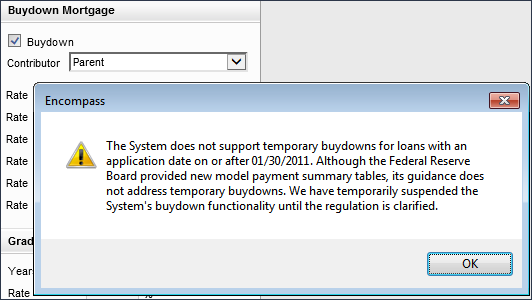

Encompass has temporarily stopped supporting temporary Buydown loans with an application date on or after January 30, 2011. Support will resume once the Federal Reserve Board clarifies how temporary Buydowns should be managed so that they comply with the Mortgage Disclosure Improvement Act (MDIA) Interim Rule for Closed-End Loans that went into effect on January 30, 2011.

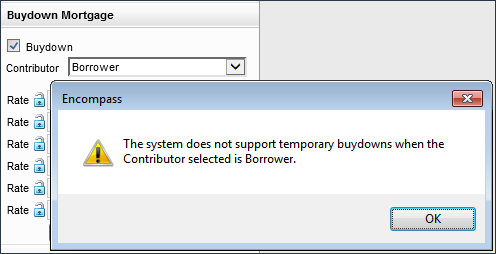

Some support for non-borrower temporary buydowns is enabled (which was introduced in Encompass 19.2 (view the release notes)). Temporary buydowns are not supported when the borrower is indicated as the buydown mortgage contributor.

It is important to note that Encompass users are still responsible for providing a Temporary Buydown Agreement as well as determining whether the terms of the temporary buydown program complies with regulatory and investor requirements.

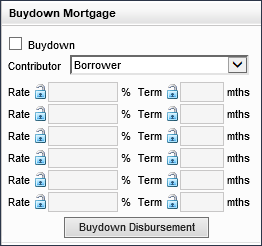

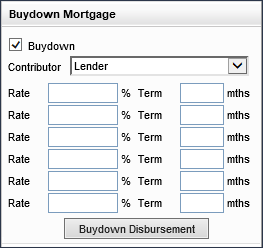

To Provide Buydown Feature Details:

- Select the Buydown checkbox to indicate the loan includes a buydown feature.

- From the Contributor dropdown list, select the individual or entity that is making contributing payments, such as the seller.

- Use the Rate and Term fields to document and calculate a borrower’s subsidized P&I payment and total buydown for loans in which the contributor is not the borrower.

- If you selected Borrower from the Contributor dropdown list:

-

The Buydown Mortgage fields are read-only by default. You may click the blue Lock icon to enter the terms of the Buydown subsidy manually. However, the REGZ-LE output form will not be accurate if it contains Buydown data and you must acknowledge that you are knowingly proceeding at your own risk before entering data.

- If you selected any other option besides Borrower from the Contributor dropdown list:

-

Enter the terms of the Buydown subsidy in the Rate and Term fields.

- Click the Buydown Disbursement button to view a quick-entry window that displays the Buydown Disbursement Summary fields. Here you can view and edit the buydown values. Any changes made in this quick entry window will be applied to the Buydown Disbursement Summary form and vice versa.

-

Users must be authorized to access the Buydown Disbursement Summary input form (via their persona) in order to view the Buydown Disbursement Summary quick entry window. Unauthorized users will receive a message stating that they cannot view the quick entry window when they click the Buydown Disbursement button.

Regarding loan templates, please note the following:

- Loan Programs Templates - When applying a Loan Programs template, values from the template for the Buydown Mortgage rates and terms will not be applied when any option besides Borrower is selected for the Contributor in the loan file.

The Contributor dropdown field has not been integrated into Loan Programs templates. Therefore, the Buydown Mortgage fields in the template are fields 1269-1274 and 1613-1618 which are used for the loan only when Borrower is selected as the Contributor.

Therefore, if you apply a Loan Programs template, the Buydown Mortgage fields in the template will be applied only when Borrower is selected as the Contributor in the loan file.

- Data Templates - The Contributor dropdown field has been integrated into Data templates (for the RegZ-LE and RegZ-CD input forms). Therefore, the Buydown Mortgage fields used for Borrower and Non-Borrower (fields 4535 - 4546) contributors are both provided in the template and values and can be entered for both types. Therefore, the values entered in the Data template for the Buydown Mortgage fields will be applied as expected for both Borrower and Non-Borrower contributors.

- Loan Programs Templates - When applying a Loan Programs template, values from the template for the Buydown Mortgage rates and terms will not be applied when any option besides Borrower is selected for the Contributor in the loan file.

As mentioned earlier, temporary buydowns were not supported in Encompass 19.1 (and later). With this in mind, on the RegZ - LE and RegZ – CD, when a user selected the Buydown checkbox (field ID 425) and then clicked a Lock icon to change any of the Rate or Term fields, the system displayed the following pop-up message.

Starting in Encompass 19.2, temporary buydowns are not supported only when the Borrower is selected as the Contributor. On the RegZ - LE and RegZ – CD in Encompass 19.2, when a user selects the Buydown checkbox, selects Borrower from the Contributor dropdown list, and then clicks a Lock icon to change any of the Rate or Term fields, the system displays the following pop-up message.

In the first two fields in the Adjustable Rate Mortgage section, enter the maximum percentage that the loan can adjust at the first adjustment period and the number of months from the close of the loan to when the first rate adjustment can occur.

-

In the Adj Cap field (field ID 695), enter the maximum percentage that the loan rate can change at each adjustment, after the first adjustment.

-

In the Adj Period field (field ID 694), enter the number of months between rate adjustments, after the first adjustment.

-

In the Life Cap field (field ID 247), enter the maximum percentage (above the initial note rate) that the rate can adjust during the life of the loan.

-

The Max Life Int. Rate field (field ID 2625) displays the maximum interest rate cap for the life of the loan.

Click the Get Index button to look up the current index (based on the ARM Index Type indicated on the the RegZ-LE). The Index field (field ID 688) is updated with the most current index and is used as the basis for the rate of the loan.

-

Due to a change of policy by the ICE Benchmark Administration effective September 2, 2014, all LIBOR index rates are updated one business day after the index’s effective date. LIBOR rates obtained using the Get Index button reflect the prior business day’s LIBOR rate.

The following ARM Index Types are impacted:

-

LIBOR - 1 month 1 Month London Inter-Bank Offering Rate (LIBOR)

-

LIBOR - 3 month 3 Month London Inter-Bank Offering Rate (LIBOR)

-

LIBOR - 6 month 6 Month London Inter-Bank Offering Rate (LIBOR)

-

LIBOR - 12 month 12 Month London Inter-Bank Offering Rate (LIBOR)

![]() Potential Negative Amortization

Potential Negative Amortization

Enter the terms for a negative amortization loan.

Enter the additional payment to be made every month to reduce the loan balance in the Extra Payment field (field ID 312).

The AP Table is disclosed when the periodic principal and interest payment for the loan can change after consummation, but not because of a change to the interest rate; or if the loan is a seasonal payment loan. If the periodic principal and interest payment does not change, the AP Table is not disclosed. The information disclosed in the AP Table on the Loan Estimate is disclosed in the AP Table on Closing Disclosure - Page 4 after being updated to reflect the terms of the loan at consummation.

The Adjustable Payment table includes the following entries:

-

Interest Only Payments - Read-only fields populated based on data from the loan file.

-

Optional Payments - Read-only fields populated based on data from the loan file.

-

Step Payments - Editable fields for indicating whether the loan has step payments (the default selection is No) and entering the number of payments that are made before the payment amount changes.

-

Seasonal Payments - Editable fields for indicating whether the loan has seasonal payments (the default selection is No) and entering a description.

-

Monthly Principal and Interest Payments

-

If the Yes option is selected for Interest Only Payments, the three fields in this section are populated with read-only text describing the changes and maximum payment amount for the principal and interest payments, based on data in the loan.

-

If the Yes option is selected for Optional Payments, Step Payments?, or Seasonal Payments, the three field in this section are blank and can be edited.

If the Biweekly option (field ID 423) is selected for the Amortization type, the title of this section changes from Monthly Principal and Interest Payments to Biweekly Principal and Interest Payments.

Use the Interest Accrual Options section to configure options for simple interest and 0% interest loan options.

The 0% Payment Option is used when originating down payment assistance loans for affordable housing. This field is applied to loan calculations only when a loan’s note rate (field 3) is set to 0%. The following values can be selected from the dropdown list:

-

Amortizing Payment – This value displays by default when a loan's note rate (field 3) is set to 0%.

-

No Payment with Balloon

-

No Payment – Fully Forgiven

All three options can be used with fixed rate 0% loans. For ARM loans with an initial 0% interest, Encompass calculations support only the Amortizing Payment option, however Encompass does not prevent a user from selecting one of the No Payment options on a 0% ARM loan.

Use the remaining fields in the Interest Accrual Options section to set the interest accrual parameters used to correctly calculate payment streams, finance charges, and APR.

-

Use 366 Days in Leap Year – When selected, this field is applied to calculations only if 365/365 or 365/360 is selected for the Interest Days/Days in a Year (field ID 1962).

-

Use Simple Interest Accrual – This field is used in combination with Interest Days /Days in Year and must be selected to apply simple interest calculations to the P&I payment and payment schedule when an option with 365 days (365/365, 365/360) is used. If this checkbox is not selected, a default value of 360/360 (standard accrual method) is used for calculations regardless of the selection made for the Interest Days/Days in a Year (field ID 1962).

-

Number of Days (Biweekly, Interim Interest Classic HELOC) – Selections in this field affect interim interest collected at closing, as well as biweekly payment schedules and classic HELOC schedules that are not configured using the HELOC Management input form.

If the Use Simple Interest Accrual checkbox (field ID 4749) is selected, the selections for the Interest Days/Days in a Year dropdown list (field ID 1962) and the Use 366 Days in a Leap Year checkbox (field ID 4748) are used to determine the simple interest calculations for the payment schedule, according to the logic in the table below.

| Interest Days/ Days in a Year | Use 366 Days in Leap Year |

Description |

|---|---|---|

| 365/365 | Selected |

Every year is calculated as 365, except for leap years, which are calculated as 366. Monthly interest is calculated on the actual days in the prior month. |

| 365/365 | Cleared |

Every year is calculated as 365, including leap years. Monthly interest for each payment is calculated based on the actual days in the prior month. |

| 365/360 | Selected or cleared |

The days per year are always 360 in this method. Monthly interest for each payment is calculated based on the actual days in the prior month. |

The Use 366 Days in a Leap Year option is applied to calculations only when the Use Simple Interest Accrual checkbox has also been selected.

![]() Adjustable Interest Rate (AIR) Table

Adjustable Interest Rate (AIR) Table

The AIR Table is disclosed when the loan’s interest rate can change after consummation. The AIR table displays on the input form when the ARM option is selected for the Amortization Type (field ID 608). If the ARM option is not selected: the loan’s interest rate does not change after consummation, the AIR Table is not disclosed, and the table does not displayed on the input form.

The AIR table includes the following entries:

-

Index + Margin - The margin index and rate.

-

Initial Interest Rate -The initial interest rate for the loan.

-

Min/Max Interest Rate - The minimum and maximum interests rates during the life of the loan. Click the Lock icon to edit the minimum rate.

-

Change Frequency - This sections display the timing of the first interest rate adjustment and the number of months between each subsequent adjustment.

-

Limits on Interest Rate Changes - The maximum interest rate change for the initial increase and subsequent increases.

For more information about construction loans, refer to the Process a Construction Loan topic.

Select a method for calculation of interest. Method A (also known as Half Loan or On Advance When Made Method): Interest is payable only on the amount advanced for the time it is outstanding. Assumes one half of the commitment amount is outstanding at the contract interest rate for the entire construction period. Method B (also known as Full Loan): Interest is payable on the entire amount regardless of actual dates or amounts of disbursement. Assumes the entire commitment amount is outstanding at the contract interest rate for the entire construction period.

Select a method for calculation of the repayment schedule. In each option, the first value represents the number of days per year used to calculate the loan's total interest and the second number represents the number of days per year used to calculate the daily interest. 360/360: Total interest is calculated based on the months in the loan period multiplied by 30 (partial months are not allowed) / Daily interest is calculated based on 360 days in a year. 365/360: Total Interest is calculated based on the total days in the loan period (partial months are allowed) / Daily interest is calculated based on 360 days per year. 365/365: Total Interest is calculated based on the total days in the loan period (partial months are allowed) / Daily interest is calculated based on 365 days per year.

- Click the Edit icons to calculate the mortgage insurance premium and term. For detailed instructions, refer to Calculating Mortgage Insurance Premiums and Payments.

Select the Prepaid checkbox to apply the months of PMI premiums (field 1209) to the payment stream in the Payment Schedule section. The prepaid premiums are applied at the end of the payment stream and reduce the PMI payment period by the same number of months.

The Projected Payments section shows the estimated payments (monthly or biweekly, depending on the loan type), the final balloon payment, if any, and the estimated monthly taxes, insurance, and assessments.

-

Click the View Payment Schedule button in the section header to view the payment schedule.

The Project Payments table is read-only by default and displays information based on the type of loan. Use the Customize checkbox and Edit button at the top of the section to customize the Projected Payments section for construction loans and other loan types that require specialized setup for the Projected Payments table.

The top of the section lists the estimated payments (monthly or biweekly, depending on the loan type). A column on the left lists the type of information displayed in each row:

-

Time period

-

Principal and interest

-

Mortgage insurance

-

Estimated escrow

-

Total estimated monthly or biweekly payment

Up to four columns on the right display payment amounts, including payments for various time periods when the principal and interest payment change, mortgage insurance payments end, or a balloon payment is due.

For example:

-

A 30-year fixed rate loan displays only one column if monthly payments do not change during the life of the loan and there is no mortgage insurance or balloon payment.

-

A 5/3 ARM Interest Only loan may have four columns due to periodic interest rate adjustments and the termination of mortgage insurance payments.

All adjustable rate (ARM) loans will generate a four column Projected Payments table based on the following loan triggers:

The final balloon payment is populated to the fourth column in the table, i.e., the Final Payment column. This is existing logic continued from earlier versions of Encompass.

-

If the Max Lifetime Rate is reached at the first adjustment, all subsequent adjustments are reflected in the four column Projected Payments table even if the payment has not changed.

-

If the Min (Floor Rate) is reached at the first adjustment, all subsequent adjustments are reflected in the four column Projected Payments table even if the payment has not changed.

![]() Periodic Principal and Interest Payment Changes

Periodic Principal and Interest Payment Changes

Four column Projected Payments table is generated when the following events occur:

-

Interest Only payment period ends

-

Negative amortization period ends

-

The anniversary of the initial periodic payment changes after multiple payment changes occur in a single year

If automatic termination of mortgage insurance occurs in any of the above scenarios, a four column Projected Payments will be generated if the current table contains only three columns. Otherwise, the automatic termination of mortgage insurance on its own will not trigger a fourth column.

The Apply Actual Payment Change checkbox is provided at the top of the Projected Payments table for ARM loans only. Select this checkbox to revert to the previous Projected Payments table trigger logic used in Encompass 15.2.0.0 (and earlier) and apply the actual payment change. This checkbox is hidden if the Projected Payments table's Customize checkbox is selected.

The Payment Schedule is calculated using values from the loan terms and loan type fields. You can also enter custom values as follows.

-

Select the Customize checkbox.

-

Type values in the Number of Payments, Interest Rate, and Monthly Payment fields as needed.

-

Click Calculate Payment to recalculate the payment schedule.

-

Clear the Customize checkbox to return to the original schedule.

These sections contain information related to loan conditions such as early payoff, late charges, and assumability.

- Click the Prepayment Penalty button to enter detailed prepayment penalty information.

![]() Enter prepayment penalty information

Enter prepayment penalty information

-

To create up to five entries for prepayment penalties, select the type of prepayment penalty (Hard or Soft).

-

Type the number of months in the prepayment period, and the percentage of the prepayment.

-

The Hard Prepayment Period and Prepayment Penalty Period fields are calculated based on previous entries.

-

In the Prepayment Penalty Fee field, enter the number of months of advanced interest that the prepay penalty cannot exceed.

-

In the Penalty Based on field, select the amount or balance on which the prepayment penalty is based.

-

When a loan is being serviced after closing, late charges established on the RegZ-LE will be adjusted on the Interim Servicing Worksheet if the amount is below the minimum or above the maximum amount configured by your administrator for the subject property state in the Servicing setting.

-

If you are using EDM or the Encompass Docs Solution, click the Get Late Fee button to automatically populate late fees based on state and agency requirements for the subject property location. The button triggers calculations that produce generic late fees or investor-driven overrides to late fees based on investor plan IDs and custom plan IDs associated with the user’s Plan ID.

-