VA Management

The VA Management form provides a convenient, central location for recording VA-related information and accessing other forms used to complete VA loans.

Most of the information in the VA Management form is automatically populated from the Borrower Summary, 1003, and VA-related forms. Click the links on the title bar on the upper-right to access information from and update content in related forms such as the 1003, GFE, and Reg-Z.

Use the Basic Information tab to record information about the borrower, subject property, and loan, as well as additional VA-related information for the loan. Most fields in the Borrower Information, Property Information, and Loan Information sections should already be completed based on entries in the Borrower Summary and 1003. Update the remaining fields with relevant information.

This section contains information related to the borrower and co-borrower.

VA Agency Case #

Enter the case number provided by the VA. (This field is auto-populated if you have already entered the information in the 1003 form.)

Veteran Information

Select the Select Borrower or Co-Borrower from the Veteran Information dropdown list to auto-populate this section with information from the 1003 and Borrower Summary forms. Enter additional information as required.

-

Select the veteran type for the borrower or co-borrower.

-

Specify if the borrower or co-borrower is using the VA loan program for the first time.

-

Enter the disability amount received, if applicable.

-

Enter the entitlement code from the VA Certificate of Eligibility. (This field is pre-populated if you have already entered the information in the VA Loan Summary form.)

VA Loan Data

Enter the borrower and co-borrower’s estimated monthly federal income tax, marital status, and veteran eligibility information.

Most of the fields in this section are read-only (not editable) and auto-populated based on entries made in the Borrower Summary and 1003 forms. Only some of the information can be updated or added.

-

Use the edit icon to recalculate the MIP/PMI/Guarantee fee and update the VA Funding Fee Amount.

-

Enter the Pest Report Fee, if applicable.

-

Click the Paid in Cash Portion link to make a secure electronic payment directly to the federal government.

Use this section to enter additional information about the property, builder, and construction details if the veteran is building or if there has been a recent construction on the property.

-

Enter the legal description of the property, usually from the title report. The information is auto-populated if it is already entered in the 1003 form.

-

Click Legal Description to access the NETROnline website for additional information related to the property. This website provides nationwide real estate research and information services such as Historical Environmental Chain of Title Reports, Condition of Title Reports, immediate access to courthouse documents (such as deeds, maps, tax data, mortgages,and so on), and access to their Public Records Online Portal.

Builder Information

Use the Builder Information section if there has been recent construction on the property or if there are upcoming plans of remodeling/construction.

-

Complete the information for the builder. Click the Address Book icon to select from your business contacts.

-

Click Builder Lookup to access the Veterans Information Portal, enter the builder’s information, and request for customized builder reports to validate the builder.

Most of the fields in this section are populated with the information from other forms such as the 1003 and Borrower Summary. Enter additional information as required.

Use the information in this tab to determine if the borrower qualifies for a VA loan.

Total Loan Amount is auto-populated from entries in the 1003 and Borrower Summary forms. To complete other fields, follow the instructions in this section.

-

Select the Yes or No checkbox to indicate if the veteran has been more than 30 days late on a payment in the last 6 months.

-

Enter a Family size.

-

Select a Country Region from the dropdown menu.

-

Next, click the Country Region field’s Lookup icon (magnifying glass) to view the residual income by region tables.

-

Using the residual income by region tables provided, locate the appropriate table based on the loan amount ($79,999 and below or $80,000 and above), and then locate the region and family size of the borrower.

-

-

Manually enter the dollar amount from the table in the for Residual Income Guidelines field

OR

Click the Get Residential Income button to populate this field automatically.

Use this section to record eligibility details. The VA Guidelines button links to the Lenders Handbook and other VA guides for reference.

-

Enter the entitlement code from the VA Certificate of Eligibility.

-

In the Base Entitlement field, enter the primary entitlement amount from the VA Certificate of Eligibility.

-

In the 2nd Tier Entitlement field, enter the second-tier entitlement amount from the VA Certificate of Eligibility.

-

In the VA County Limits field, enter the county-specific VA loan limit.

Most of the information in this section is auto-populated from the 1003 and Borrower Summary forms. Update other fields as required.

-

Click Income & Expenses to access the Quick Entry form, enter information and update the Actual column in the Ratio section with calculated debt-to-income ratios.

Use this section to enter planned costs of Energy Efficient Improvements to the subject property. These costs impact the maximum loan amount and are typically placed in an escrow account. The Energy Efficient Improvement Financed Amount and the EEM Included in Base Loan Amount checkbox are disabled by default unless the loan is a VA IRRRL loan that meets the following conditions described below.

EEM Guidelines for VA IRRRL Loans

The Energy Efficient Improvement Financed Amount is blank by default and the EEM Included in Base Loan Amount checkbox is cleared by default. Both fields are disabled by default unless the loan is a VA IRRRL loan that meets one of the following conditions:

-

A date of 08/08/2019 or later is enter for the Doc Signing Date, Mortgage Origination Date, Closing Date, or Est. Closing Date.

-

No date is entered for the Doc Signing Date, Mortgage Origination Date, Closing Date, or Est. Closing Date.

This behavior is not applied to VA IRRRL loans closed prior to 08/08/2019.

When a user selects the EEM Included in Base Loan Amount checkbox, Encompass copies the value from the Energy Efficient Improvements amount (field ID 961) to the Energy Efficient Improvement Financed Amount. This is a one-way copy. Subsequent changes to the Energy Efficient Improvements amount are also copied to the Energy Efficient Improvement Financed Amount, but changes to the Energy Efficient Improvement Financed Amount are not copied back to the Energy Efficient Improvements amount. When the checkbox is cleared, the Energy Efficient Improvement Financed Amount is also cleared.

Click the Lock icon to edit the Energy Efficient Improvement Financed Amount. This enables adjustments to the amount when not all the energy efficient improvement costs are allowable as financed amounts.

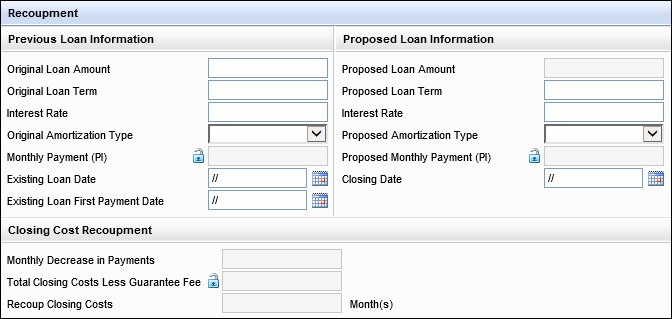

Use the Recoupment section to compare the previous loan information with the proposed new loan information for refinance loans, and to calculate the recoupment period for all allowable fees and charges financed as part of the loan or paid at closing.

This section was updated in the Encompass 19.4 release (release notes).

To Complete the Recoupment Section

-

For a refinance loan, in the Previous Loan Information section, enter the loan amount, loan term, interest rate, and existing loan date and existing loan first payment date for the previous loan, and then select the Original Amortization Type for the previous loan.

It is recommended that Encompass users review VA guidelines on how to document the existing loan data, including documentation of the rate to use for ARM loans.

-

Most fields in the Proposed Loan Information section are populated with data from other input forms. Enter the existing First Payment Date (field ID 682) and select the Rate Reduced Solely by Discount Points checkbox (field ID VASUMM.X131) if the lender has certified a reduced rate on a refinance transaction solely based on the payment of discount points.

-

In the Closing Costs Recoupment section, select the VA Loan Code for the new loan, and then select or clear the Include checkbox to include or exclude amounts from the recoupment calculation.

-

This section captures the closing costs associated with the Loan Estimate. All fields in this section can be edited by clicking the Lock icons. Costs reflected are based on the most recently disclosed Loan Estimate. If no loan estimate has been disclosed yet, this section reflects the current state of the loan fees.

-

This section captures current state of the closing costs which will be disclosed on any new Closing Disclosure. All fields in this section can be edited by clicking the Lock icons. This does not reflect the most recent disclosed value for the closing disclosure, but enables the user to address any remaining issues on the loan from a recoupment standpoint that may need to be addressed prior to closing.

-

For VA IRRRL loans, complete the Statutory Closing Cost Recoupment section as described below.

This feature was introduced in the Encompass 19.4 release (release notes).

Statutory Closing Cost Recoupment Section for VA IRRRL Loans

This section is used to populate statutory closing cost recoupment amounts for VA IRRRL loans. The fields in this section are enabled only for loans with a Loan Type (field ID 1172) of VA and a VA Loan Code (field ID 958) of VA IRRL when the loan meets one of the following conditions:

-

A date of 08/08/2019 or later is enter for the Doc Signing Date, Mortgage Origination Date, Closing Date, or Est. Closing Date.

-

No date is entered for the Doc Signing Date, Mortgage Origination Date, Closing Date, or Est. Closing Date.

This behavior is not applied to VA IRRRL loans closed prior to 08/08/2019.

To Complete the Statutory Closing Cost Recoupment Section

-

Complete the following fields before entering data in the Statutory Closing Costs Recoupment section :

-

Select the VA option for the Loan Type (field ID 1172).

-

Select the VA IRRRL option for the VA Loan Code (field ID 958).

-

Enter the Existing Loan Date (field ID NTB.X1) and the Closing Date (field ID 748) to fully calculate the recoupment costs.

-

Enter the first payment dates for the new and existing loans (field IDs 682 and VASUMM.X123) to enable the Encompass compliance service to accurately assess the loan against VA requirements.

-

-

Enter any energy efficient improvement amounts in the EEM section of the form.

-

Use the Financed Closing Costs to Exclude field (field ID VASUMM.X134) to enter any closing costs included in the base loan amount that are to be excluded from the base loan amount for purposes of evaluating the statutory P&I payment. If your company policies do not permit the exclusion of financed closing costs, this field may be disabled.

Please review VA guidelines on what financed fees are appropriate to exclude from the statutory P&I calculation.

-

The remaining fields in this section are calculated based on data entered in other fields

This tab was introduced in the Encompass 19.1 April Service Pack release (release notes)

The Cash-Out Refinance tab supports the changes mandated by VA-Guaranteed Cash-Out Refinancing Home Loans Circular 26-19-05. The form includes the following sections:

The Loan Comparison section enables the entry and calculation of loan comparison data for a proposed cash-out refinance loan and an existing loan on the subject property. Encompass captures values related to the veteran’s existing loan (the current loan being refinanced) and compares them to the proposed loan. A visual indicator on the input and output forms indicating the type of impact (Increase, Decrease, or None).

Some fields, notably the Total of the Remaining Scheduled Payments for the existing loan and the proposed loan, as well as the overall change in payments made during the life of the loan are subject to final guidance from VA and are included as data entry fields in the current phase.

The following table lists the fields used for the Loan Comparison section.

| Existing Loan (Being Refinanced) | Proposed Loan | Impact of New Loan (Amount and Change Type) |

|---|---|---|

| Loan Balance (field ID VASUMM.X102) |

Total Loan Amount (field ID 2) |

If existing loan fully paid off by refinance, reflects $0.00 and Decrease. If not fully paid off, reflects the difference between existing loan and total loan amount to reflect the actual dollar amount decrease. (Field IDs VASUMM.X103 and VASUMM.X116) |

| Remaining Term (field ID NTB.X4) |

Loan Term (field ID 4) |

If new term is longer than existing term (example: current remaining term is 300 months, new term is 360), the impact will reflect

-60 and Increase. |

| Interest Rate (field ID NTB.X7)

NOTE: For other VA products (i.e. VAIRRRL) the current rate must still be entered in field ID VASUMM.X16, which is the Interest Rate used on the Qualification tab. |

Rate (field ID 3) | If the rates are equal, will reflect 0 and None. Otherwise will reflect the amount of the difference and Increase or Decrease.

(Field ID VASUMM.X105 and VASUMM.X118) |

| Total of Remaining Scheduled Payments (field ID VASUMM.X106)* | Total of Remaining Scheduled Payments (field ID VASUMM.X107)* | If the amounts are equal, will reflect 0 and None. Otherwise will reflect the amount of the difference and Increase or Decrease.

(Field ID VASUMM.X108 and VASUMM.X119) |

| LTV (field ID NTB.X17) | LTV (field ID 353) | If the amounts are equal, will reflect 0 and None. Otherwise will reflect the amount of the difference and Increase or Decrease.

(Field IDs VASUMM.X109 and VASUMM.X120) |

| Reasonable Value (field ID VASUMM.X110) | Appraised Value (field ID 356) | Discuss with your internal compliance department whether the current appraised value or the appraised value at the time of origination of the loan being refinanced should be documented as the reasonable value. |

| Remaining Equity (field ID VASUMM.X111).Calculated as (field ID VASUMM.X110) - Existing Liens (field ID 26) |

Remaining Equity (field ID VASUMM.X112) Calculated as Appraised Value (field ID 356) -Existing Liens (field ID 26) | The remaining equity is assessed based on the provided valuation less the mortgage and HELOC payoffs associated with the subject property for both the loan being refinanced and the proposed loan. Impact will reflect Increase, Decrease, or None based on the comparison. (Field IDs VASUMM.X113 and VASUMM.X121) |

*Guidance from VA is incomplete and expected to change on these fields. For the Encompass 19.1 April Service Pack release, the Total of Remaining Scheduled Payments fields are being released as manual entry, with a calculated comparison between the fields. Lenders should review and consult with their internal compliance experts to assess appropriate procedures and controls.

The required comparison for VA Cash-Out Refinance includes existing and new Net Tangible Benefit (NTB) tests to be executed on the new loan. In line with the existing design of the Net Tangible Benefit tool in Encompass, these fields are not automatically calculated and should be reviewed by the lender. The Net Tangible Benefit table on the Cash-Out Refinance tab includes eight checkboxes that consolidate and expose all required tests.

The following table lists the Encompass field IDs for the Net Tangible Benefit checkboxes.

| Field ID | Description |

|---|---|

| NTB.X45 | The new loan eliminates monthly mortgage insurance, whether public or private, or monthly guaranty insurance. |

| NTB.X68 | The term of the new loan is shorter than the term of the loan being refinanced. |

| NTB.X37 | The interest rate on the new loan is lower than the interest rate on the loan being refinanced. |

| NTB.X38 | The payment on the new loan is lower than the payment on the loan being refinanced. |

| NTB.X69 | The new loan results in an increase in the borrower’s monthly residual income as explained by 38 CFR 36.4340(e). |

| NTB.X70 | The new loan refinances an interim loan to construct, alter, or repair the primary home. |

| NTB.X71 | The new loan amount is equal to or less than 90 percent of the reasonable value of the home. |

| NTB.X40 | The new loan refinances an adjustable rate mortgage to a fixed rate loan. |

VA-Guaranteed Cash-Out Refinancing Home Loans Circular 26-19-05 requires the Lender to disclose to the borrower the amount of home equity being removed from the home as a result of the new loan within three (3) business days from the initial date of the loan application and at loan closing. An estimated amount field (field ID VASUMM.X113) was created for this purpose.

The Refinance Closing Summary section provides the borrower with a summary of the proposed refinance loan benefits and costs.

Three new fields were created for the Refinance Closing Summary section.

-

Amount of Cash Directly Disbursed to Borrower(s) (field ID VASUMM.X114) – If the Cash to Borrower (field ID 142) is 0 (zero) or a positive amount, then 0 is populated to this field. If the Cash to Borrower (field ID 142) is a negative amount, a corresponding positive amount is populated. For example, if the Cash to Borrower is -5.00, the Amount of Cash Directly Disbursed to Borrower(s) is populated with 5.00.

-

Payoffs Disbursed, Excluding Mortgages, on Behalf of Borrower(s) (field ID VASUMM.X115) – For Standard Disclosures, this field is populated with the Third Party Payments Not Otherwise Disclosed (field ID LE2.X29) minus any Existing Lien (field ID 26) on the property. For Alternate disclosures, this field is populated with the Estimated Total Payoffs and Payments (field ID LE2.X31) minus any Existing Lien (field ID 26) on the property.

-

Amount of Increase in Total Paid Over Life of Loan (field ID VASUMM.X122) – The amount of any Increase in the total paid over the life of the loan. Guidance from VA is incomplete and expected to change on this field. For the Encompass 19.1 April Service Pack release, this field is being released as manual entry. Review and consult with your internal compliance experts to assess appropriate procedures and controls.

![]() Recoupment Section and Refinance Type

Recoupment Section and Refinance Type

One field was created for the Previous Loan Information sub-section in the Recoupment section:

-

Existing Loan First Payment Date (field ID VASUMM.X123) - Date field where the borrower's existing first loan payment date can be entered. The Encompass Compliance Service (ECS) reviews will use this value to calculate the borrower's VA loan seasoning requirements when determining if the loan qualifies for a streamline refinance.

Use the Refinance Type section to select a refinance type (field ID VASUMM.X125):

-

TYPE I Cash-Out Refinance - The loan amount (including VA funding fee) does not exceed the payoff amount of the loan being refinanced.

-

TYPE II Cash-Out Refinance - The loan amount (including VA funding fee) exceeds the payoff amount of the loan being refinanced.

For VA Refinances originated as Type 1, Encompass perform a different recoupment cost set of calculations. This test is not run on Type 2 cash-out refinance. If the loan is Type 2, the fields reflect blank for decrease in payments and recoupment. This section does not impact the calculations or the input form for VA IRRRL, which remains on the Qualification tab on the VA Management form.

The table below shows the Closing Cost Recoupment calculations.

| Field | Calculation | Comments |

|---|---|---|

| Monthly Decrease in Payments (field ID VASUMM.X22) |

Type 1

Type 2

The previous calculation logic for monthly decrease in payments is being used for VAIRRL loans. |

P&I comparison only. The test for Type I excludes PITI and prepaids automatically. These are still options for VAIRRL. |

| Total Closing Costs Less Guarantee Fee (field ID VASUMM.X124) |

Field ID VASUMM.X25 – field ID 969 | Existing Closing Costs calculation for VA does not exclude funding fee. This is a new requirement for the cash out refinance test. |

| Recoup Closing Costs Months (field ID VASUMM.X27) |

Type 1

Type 2 The previous calculation logic for recoup closing costs months is being used for VAIRRL loans. |

Applies to Type 1 transactions with application dates on or after 2/25/2019. |

Use the information in this tab to track the dates and events associated with the VA loan.

-

In the Staff Appraisal Reviewer (SAR) section, enter the SAR’s details such as name, ID, and LAPP certification.

-

In the Notice of Value (NOV) section, enter the details of the SAR’s appraisal such as when the appraisal was sent, NOV was received, issued, and so on.

-

In the Certificate of Eligibility section, enter the COE details such as when the certificate was ordered, when it was issued, and the order history.

-

In the Funding Fee section, enter the VA loan details such as when the loan was received and if there was a document of receipt associated with the payment.

-

In the Other Important Dates section, enter information such as when the Loan Guarantee Certificate was received, Certificate of Commitment was issued by VA, and so on.

-

Click MERS MIN to automatically populate the MERS Registration field, if your Encompass admin has configured your system for automatic MERS MIN number generation. Else, enter the information manually.

-

Click GSA Search to access the System for Award Management (SAM) website.

-

-

In the CAIVRS section, enter the Credit Alert Verification Reporting System (CAIVRS) details associated with the loan.

-

Click Obtain to access the FHA Connection website.

-

-

In the Insurance Policies section, select checkboxes to indicate if flood, hazard, wood, and wind insurance policies have been purchased.